.avif)

Blog Summary

- What outsourced payroll providers in the UK actually do and who they are right for

- The real difference between a fully managed payroll service and a payroll bureau

- The key benefits of outsourcing payroll and which ones matter most for accounting practices

- Five criteria for evaluating providers, with a side-by-side comparison of the main models

- How Finqube gives your practice visibility and control without the cost of hiring in-house

Introduction

Most practice owners who start looking at outsourced payroll providers in the UK are not doing it because payroll has become too expensive. They are doing it because payroll has become too unreliable.

A late FPS submission. A PAYE liability that does not reconcile correctly. An employee who left in June but is still showing on payroll records in July. Individually, these issues are usually fixable. The problem is the cumulative effect. Every correction creates additional administration, client conversations, and avoidable compliance risk for the practice.

This guide covers everything you need to evaluate outsourced payroll providers in the UK properly: what the different models actually are, what they cost, what the genuine benefits are, and how to tell the providers worth working with from the ones who just move the problem elsewhere.

What Is Outsourced Payroll and Who Is It For?

Outsourced payroll means transferring the day-to-day processing and compliance administration of client payrolls to a specialist provider. Depending on the service model, the provider may handle payroll calculations, payslip production, Full Payment Submission (FPS) and Employer Payment Summary (EPS) filings to HMRC, PAYE reconciliations, pension assessments, opt-out processing, and submissions to workplace pension schemes. Most providers operate within recognised payroll software such as Xero Payroll, BrightPay, Sage Payroll, or Moneysoft.

For UK accounting practices, there are two situations where this becomes relevant. The practice is growing and payroll volume is outpacing the team's capacity. Or payroll accuracy is becoming a reputational risk because the current process has no structured review layer.

Both are capacity problems. The solution is not always the same. Which model you choose depends on how much ownership you need the provider to take.

Fully Managed Payroll vs Payroll Bureau: What Is the Difference?

This is the question that most comparisons skip past. It matters more than which software a provider uses or how many payrolls they process per month.

The distinction matters because many providers market themselves as fully managed when they are operating as a bureau. The test is simple: ask them what their process is when a client sends incomplete data three days before the RTI deadline. If the answer is that they process what they have and flag it after, that is a bureau. If the answer describes a chase process and a pre-filing review, that is a managed service.

For most accounting practices, a payroll bureau creates a different kind of administration rather than removing it. The practice still coordinates data intake, checks for errors, and resolves issues. The processing has moved. The responsibility has not.

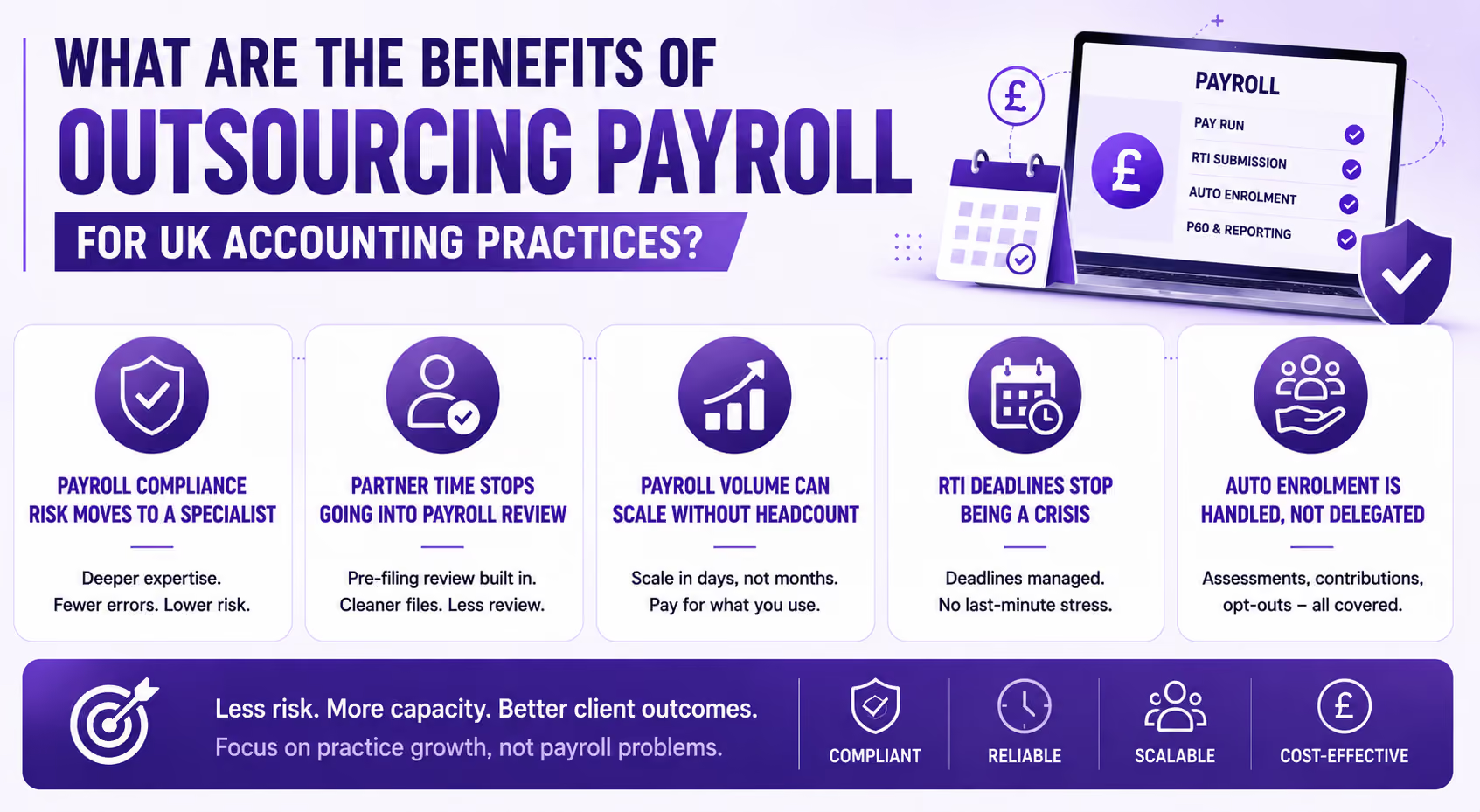

What Are the Benefits of Outsourcing Payroll for UK Accounting Practices?

The benefits that get listed most often are cost savings and time savings. Those are real, but they are not the primary reason experienced practice owners make the switch. The deeper benefits are about risk and capacity.

Payroll compliance risk moves to a specialist

RTI penalties, auto enrolment non-compliance, and P60 errors are not catastrophic individually. But each one costs time to resolve and creates a client conversation you do not want to have. A specialist payroll team running your client payrolls carries deeper compliance knowledge than a generalist accounting team processing payroll alongside everything else. The error rate goes down.

Partner time stops going into payroll review

In most practices, partners end up reviewing payroll because nobody else has the authority to sign off a client-facing output. That is expensive. A fully managed provider with a structured pre-filing review built into their process reduces the review burden significantly. The partner sees a clean file, not a raw output.

Payroll volume can scale without headcount

Hiring a payroll administrator takes 3 months and carries a fixed cost. Scaling with an outsourced provider takes days and scales with volume. For practices growing their client base, that flexibility has a direct impact on profitability.

RTI deadlines stop being a crisis

Payroll deadlines extend beyond submitting RTI data on time. Practices also need to ensure PAYE and National Insurance liabilities are paid by the 19th of the month for postal payments or the 22nd for electronic payments. A well-structured payroll provider maintains both filing and payment workflows, reducing the risk that deadlines become dependent on a single team member or partner being available at the right time.

Auto enrolment is handled, not delegated

Auto enrolment remains one of the most overlooked payroll compliance responsibilities. Providers must assess worker eligibility, process opt-outs within statutory timeframes, calculate contributions correctly, manage re-enrolment duties, and maintain compliance with The Pensions Regulator's requirements. Variable-pay employees often create the greatest challenge because eligibility can change from one pay period to the next. A managed payroll service should handle these processes as part of its standard workflow rather than leaving them for the practice to monitor manually.

Why Do Accounting Practices Struggle with Payroll in-House?

Payroll looks manageable until it is not. A practice processing 20 client payrolls in 2021 may be processing 60 by 2024, with the same team. The work has not scaled. The team has.

The problems that come up most consistently are these:

- Payroll processing takes 2 to 3 days per pay cycle but clients treat it as a same-day turnaround

- RTI deadlines are fixed. They do not move when a staff member is off sick or client data arrives late

- Auto enrolment errors are not caught until the pension provider flags them, often months later

- Partners end up reviewing payroll themselves because there is no intermediate check in the process

Most growing practices encounter these pressures at some stage. The underlying issue is rarely capability. More often, payroll volume and compliance obligations have expanded faster than the systems and resources supporting them.

Who Is Responsible for Payroll Compliance When You Outsource?

This is the question most practice owners do not ask until something goes wrong.

When you outsource payroll to a provider, the provider is responsible for accurate processing based on the data you supply. You remain the accountable party to your client. If a provider files an incorrect RTI submission, the client relationship issue lands with your practice, not the provider.

This matters when choosing a provider. The question is not just whether they process payroll accurately. The question is whether you can see what they are doing before it is filed.

A provider that gives you visibility before submission protects you. One that sends a confirmation after filing does not.

When Does It Make Sense to Outsource Payroll?

If any of the following are true for your practice, you have already passed the point where outsourcing makes sense:

- Your team is processing more than 15 client payrolls per month alongside their other work

- You have had a payroll error reach a client in the last 12 months

- A payroll deadline has been missed or filed late under RTI

- A partner is spending time reviewing payroll that a trained payroll person should be handling

- Auto enrolment assessments are being done manually rather than through a system

These are not failure signals. They are growth signals. The practice has outgrown its current payroll setup.

Where Do Most Payroll Errors Happen in UK Accounting Practices?

Based on what Finqube sees across client engagements, the errors cluster in three places.

Data handoff between client and practice

Clients send payroll data late, in the wrong format, or with starters and leavers missing. Without a structured intake process, these gaps are not caught until after processing.

RTI submissions with no pre-filing reconciliation

RTI submissions filed without reconciliation checks frequently allow small discrepancies to persist across multiple pay periods. An incorrect tax code, an employee marked as active after leaving, or a PAYE variance left unresolved can continue unnoticed until year-end reporting or an HMRC query highlights the issue.

Auto enrolment assessments on variable pay

Workers with variable earnings are frequently misassessed for auto enrolment eligibility. This creates pension compliance issues that take significant time to unwind.

How to Choose the Right Outsourced Payroll Provider in the UK

There are five criteria that separate a provider who reduces your risk from one who just moves it.

1. Review Visibility Before Filing

You need to see work before it goes to HMRC. This is not a nice-to-have. A provider who sends you a confirmation after filing is asking you to trust the output without the ability to check it. Ask directly: what does your pre-filing review process look like and what access do I have to it?

2. RTI Compliance Track Record

Any provider worth evaluating should be able to explain how they monitor filing accuracy, manage corrections, and track compliance performance. Ask how they handle FPS and EPS submissions, what review steps take place before filing, and how discrepancies are escalated. HMRC penalties for late or inaccurate RTI submissions are measurable. The reputational impact on the accounting practice is often far greater.

3. Auto Enrolment Depth

Auto enrolment is not optional and it is not simple. Variable pay workers, multiple employment situations, postponement assessments, opt-out processing. A provider who handles RTI filing but leaves auto enrolment to your team has not taken payroll off your plate.

4. PAYE Reconciliation

A PAYE reconciliation check each period is the difference between a clean year-end and a corrective FPS sprint in March. Ask whether reconciliation is built into their standard process or a separate engagement.

5. System Compatibility

If your practice runs on Xero and the provider needs you to export data into a spreadsheet, the admin burden has not gone away. It has just changed shape. A good provider works inside your existing systems.

Comparing Outsourced Payroll Provider Types

Not all outsourced payroll providers in the UK operate the same way. Here is how the main models compare across the criteria that matter most.

How Finqube Supports Outsourced Payroll for UK Accounting Practices

Finqube provides UK accounting practices with a dedicated remote accountant who works inside your existing systems and takes full ownership of payroll from data intake to RTI filing.

Every Finqube engagement includes access to our proprietary AI review software. Before an RTI submission goes to HMRC, the software has already run a reconciliation check against the prior period, flagged any discrepancies, and given you a clean file to approve. You review what has already been checked. You are not the first line of review. You are the final sign-off.

- Dedicated payroll accountant deployed in 1 to 2 weeks

- Works inside your Xero, QuickBooks, Sage, or FreeAgent setup

- RTI submissions reviewed before filing, not confirmed after

- Auto enrolment assessments included as standard

- One-month free pilot, no contract

You can compare the cost against hiring in-house on our ROI calculator at finqubeaccounting.com.

One month. No contract. See how it works before you decide.

Start your free pilot at finqubeaccounting.com

One month. No contract. See how it works before you decide.

Start your free pilot at finqubeaccounting.com

Book a Free Call

Conclusion

Choosing between outsourced payroll providers in the UK comes down to understanding what you actually need: a bureau that processes data you send, or a fully managed service that takes the full payroll cycle off your plate.

If payroll is becoming a capacity problem or a compliance risk, the bureau model rarely solves it. It moves the processing but leaves the coordination, the review, and the deadline pressure with your practice.

A fully managed provider who works inside your systems, reviews before filing, and covers auto enrolment as standard removes the problem at the source. The benefits are real, the costs are calculable, and the difference in outcomes is significant.

Frequently Asked Questions

How much does payroll outsourcing cost in the UK?

Payroll bureau costs typically range from GBP 2 to GBP 8 per employee per month, excluding auto enrolment. Accountancy firm payroll teams generally charge a fixed fee per client payroll, often GBP 150 to GBP 500 per month depending on employee count. Fully managed remote models like Finqube work on a fixed monthly fee that covers payroll alongside other accounting support. The right comparison is total cost of delivery, not the headline per-payslip rate, because bureau pricing rarely includes auto enrolment or pre-filing review time.

What are the main benefits of outsourcing payroll for an accounting practice?

The primary benefits are compliance risk reduction, recovered partner time, scalable capacity, and consistent RTI deadline delivery. The benefit that gets underestimated most is auto enrolment coverage. Practices that outsource payroll to a fully managed provider eliminate the quiet compliance risk that builds up when variable pay workers are manually assessed and pension submissions are handled separately from payroll processing.

Who is liable if an outsourced payroll provider makes an error?

The accounting practice remains accountable to the client relationship even when payroll processing is outsourced. If an FPS or EPS submission is incorrect, HMRC correspondence is issued to the employer and the practice is often expected to coordinate the resolution. This is why visibility, audit trails, reconciliation procedures, and documented review processes matter as much as processing capacity when selecting a payroll provider.

A provider with a pre-filing review process reduces the probability of errors reaching HMRC. Confirm in your service agreement where liability sits for processing errors versus errors caused by incorrect data from the client.

How long does it take to set up outsourced payroll with a new provider?

Bureau-style providers typically take 4 to 8 weeks to onboard a payroll due to data migration requirements. A dedicated remote accountant working inside your existing software can be processing payrolls within 1 to 2 weeks because no migration is needed. They work in your environment from day one.

What should I ask an outsourced payroll provider before signing?

Ask four questions. First, what is your RTI error rate and how is it measured? Second, what is your process when a client sends incomplete data before the deadline? Third, is auto enrolment included or charged separately? Fourth, can you work inside our existing Xero, QuickBooks, or Sage environment without us exporting data? A provider who cannot answer these clearly is unlikely to reduce your risk.

Is outsourced payroll right for a small accounting practice?

It depends on volume and error history, not size. A practice with 10 to 15 client payrolls and no errors or deadline issues may not need to outsource. A practice with the same volume and a pattern of last-minute corrections, missed deadlines, or partner review involvement should be looking at a managed service. The trigger is not headcount. It is whether payroll is consuming time that should be going elsewhere.